Sensex Down 114 Points, Nifty at 24,326; Tomorrow Nifty Prediction

Market Closes in the Red: A Deep Dive into the May 7 Performance and Outlook for May 8

The Indian equity markets navigated a turbulent landscape on Thursday, ultimately succumbing to a marginal decline as investors grappled with a cocktail of domestic earnings and shifting geopolitical narratives. While the headline indices painted a picture of stagnation, the underlying market breadth told a more nuanced story of resilience in the broader market.

The Numbers: A Day of Consolidation

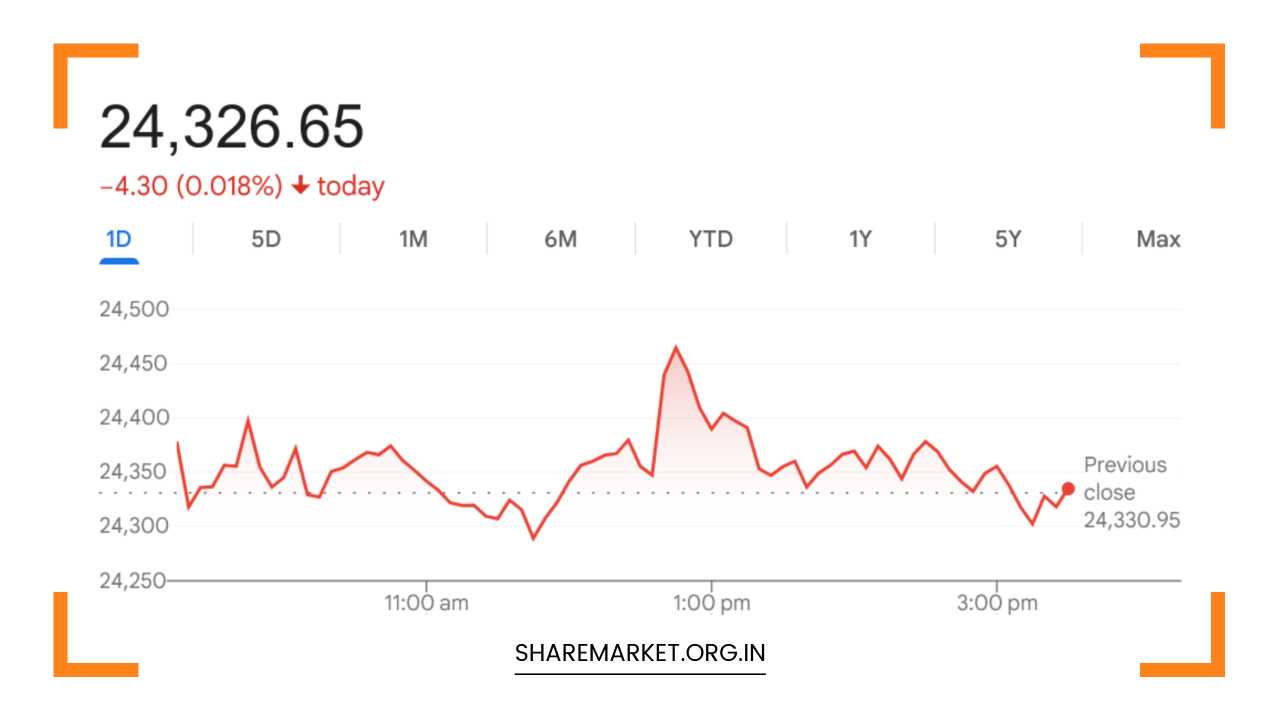

Indian benchmark indices remained subdued throughout Thursday’s trading session. Amidst bouts of volatility, the Nifty 50 managed to defend the 24,300 psychological level, though it struggled to find a definitive upward catalyst.

-

Sensex: The BSE Sensex shed 114 points (0.15%) to settle at 77,844.52.

-

Nifty 50: The NSE Nifty declined by a fractional 4.30 points (0.02%) to close at 24,326.65.

Despite the red close for the “heavyweights,” the broader market significantly outperformed. The Nifty Midcap index rose by 1.1%, while the Smallcap index climbed 0.9%, suggesting that risk appetite remains healthy among retail and institutional investors in the second-tier segments.

Sectoral Dynamics: The Tug-of-War

The day was characterized by a sharp divide between “Old Economy” sectors and “Growth/Consumption” plays.

The Gainers (Auto, Defense, Metals)

Buying interest was concentrated in sectors with strong structural tailwinds.

-

Auto: Led by Bajaj Auto and Mahindra & Mahindra, the sector benefited from positive sentiment surrounding rural demand and premiumization.

-

Defense & Metals: Strategic interests and a stabilization in global commodity prices provided a floor for these counters.

-

Top Nifty Gainers: HDFC Life Insurance, Bajaj Auto, M&M, Grasim Industries, and NTPC.

The Losers (IT, FMCG, Banks)

Conversely, “safe haven” sectors and interest-rate-sensitive stocks faced selling pressure.

-

IT & FMCG: Giants like TCS, Tech Mahindra, and Hindustan Unilever (HUL) weighed on the index. Concerns over global discretionary spending and sluggish volume growth in rural FMCG markets continue to haunt these sectors.

-

Consumer Durables: High valuation concerns led to profit-booking in stocks like Titan Company.

-

Top Nifty Losers: Tech Mahindra, HUL, Titan, TCS, and ITC.

Geopolitical Jolts: The “Hormuz” Factor

One of the primary drivers of intraday volatility was the fluctuating news flow regarding the Middle East. Early reports suggested a potential agreement between the US and Iran to ensure the stability of the Strait of Hormuz, a critical chokepoint for global oil transit.

This news initially sent crude oil prices dipping below $100 per barrel, providing a momentary relief rally for oil-importing nations like India. However, as uncertainties regarding nuclear enrichment discussions resurfaced, the “peace dividend” evaporated. Investors quickly pivoted to profit-booking as the prospect of a sustained dip in energy costs became less certain.

Expert Technical Perspectives

Technical analysts suggest that while the day was quiet, the structural setup remains constructive.

1. The Bullish Breakout Theory

Rupak De, Senior Technical Analyst at LKP Securities, highlights that the Nifty has witnessed a consolidation breakout on the daily timeframe.

-

RSI: The Relative Strength Index is exhibiting a bullish crossover.

-

Moving Averages: The index has moved above its 50-day Exponential Moving Average (EMA), a classic signal that the intermediate trend is shifting from bearish to cautiously optimistic.

-

Target: De expects the Nifty to advance toward the 24,750–24,800 range, provided the 24,200 support level holds.

2. The Momentum Stall

Sudeep Shah of SBI Securities offers a more tempered view. He notes that Thursday saw the Nifty trade within a narrow 198-point range—its tightest in seven sessions.

“The formation of a small-bodied candle with an upper shadow signals mild profit-booking at higher levels. While we are above the 20-day and 50-day EMAs, the RSI remains in a sideways zone, indicating a lack of ‘firepower’ for a vertical breakout.”

Macro View: Domestic Resilience vs. Global Cues

Vinod Nair, Head of Research at Geojit Investments, points out that the domestic market is currently caught between two worlds. While the Indian Rupee has shown strength, providing a cushion against imported inflation, global cues remain mixed.

The focus is now shifting heavily toward the Q4 earnings season. Management guidance will be the “make or break” factor for large-cap stocks. If corporate India can demonstrate that margins are being protected despite high interest rates, we could see a fresh leg of the rally.

What to Expect on May 8

As we head into the final trading session of the week, several key factors will dictate the opening bell:

| Factor | Impact | Monitor |

| Crude Oil | High | Any breach back above $105/bbl will be bearish for OMCs and Paints. |

| US Markets | Medium | Overnight performance of the Nasdaq will dictate the opening for Indian IT. |

| FII Activity | High | Foreign Institutional Investors have been net sellers; a reversal is needed for a 24,500+ move. |

| Q4 Results | Very High | Stock-specific movements based on late-evening earnings releases. |

Abhinav Tiwari, Research Analyst at Bonanza, emphasizes that the market will remain “stock-specific.” In an environment where the macro-picture is hazy due to the Middle East, investors are likely to cluster around companies with visible earnings growth.

Strategic Outlook for Traders

For the session on May 8, the strategy should be “Buy on Dips” near the 24,200 mark, with a strict stop-loss.

-

Upside Resistance: 24,450 and 24,600.

-

Downside Support: 24,200 and 24,050.

The market is currently in a ‘wait-and-watch’ phase. While the underlying trend is robust, the lack of immediate momentum suggests that patience will be a more profitable virtue than aggressive chasing. Investors should keep a close eye on the Auto and Metal sectors for continued strength, while exercising caution in the IT space until the global outlook clarifies.

Final Thoughts

Thursday’s minor decline is best viewed as a breather in a larger recovery trend. The “Red” close is less of a warning sign and more of a consolidation phase as the market digests geopolitical news and prepares for the next set of earnings data. For May 8, stability in crude prices and steady global markets could easily propel the Nifty back toward its recent highs.