Sensex Down 465 Points. Nifty at 25,722; Nifty Prediction for Monday

Market Wrap-Up: Indices Close in the Red as Investors Book Profits

Find out how markets might behave on November 3rd.

The Indian stock market ended the last trading day of the week on a weak note, breaking its four-week winning streak. On Thursday, October 31st, the Sensex and Nifty both slipped into the red amid widespread profit-booking, global uncertainty, and sector-specific weakness. After a strong month-long rally that lifted benchmark indices to record highs, investors appeared to take a breather, locking in gains and reducing exposure ahead of the weekend.

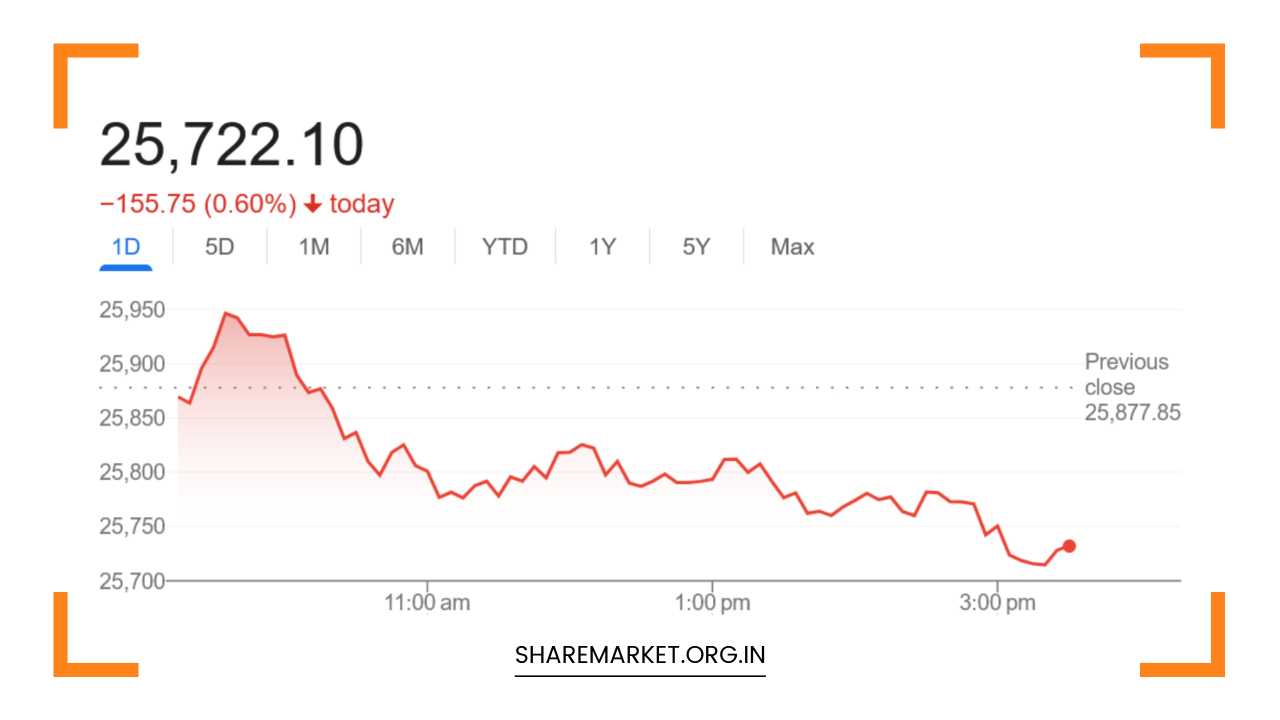

At the close of trade, the BSE Sensex fell 465.75 points, or 0.55%, to settle at 83,938.71, while the NSE Nifty 50 declined 155.75 points, or 0.60%, to end at 25,722.10. The broader market indices mirrored this negative sentiment, with both midcap and smallcap segments seeing notable declines. The BSE Midcap index fell around 0.8%, while the Smallcap index slipped by nearly 1%, suggesting that investors were trimming positions across the board.

Sectoral and Stock Performance

Sector-wise, the market showed a mixed pattern. Heavy selling was observed in metal, pharma, and information technology (IT) counters, while selective buying was visible in public sector banks (PSU banks) and defense-related stocks.

Out of the 30 Sensex constituents, 25 ended in the red, while 41 out of 50 Nifty stocks also witnessed selling pressure. Within the Bank Nifty, 6 out of 12 components declined, reflecting mild weakness in the banking space despite gains in PSU names.

On the Nifty gainers list, Bharat Electronics, Eicher Motors, Shriram Finance, Larsen & Toubro (L&T), and Tata Consultancy Services (TCS) stood out. Bharat Electronics gained traction following continued optimism in the defense sector and strong quarterly earnings, while Eicher Motors advanced on expectations of robust festive season demand.

On the flip side, Cipla, Eternal, Max Healthcare, NTPC, and Interglobe Aviation (IndiGo) were among the top laggards. Pharma stocks came under pressure due to concerns about pricing challenges in the US market, while NTPC and Interglobe saw profit-taking after recent gains.

Despite the weakness in indices, market breadth on the Bombay Stock Exchange (BSE) was relatively healthy, with over 170 stocks touching their 52-week highs. Notable names included Navin Fluorine, Chennai Petro, IDBI Bank, IDFC First Bank, Canara Bank, Punjab National Bank (PNB), Bank of India, Bank of Baroda, HPCL, RBL Bank, Indian Bank, State Bank of India (SBI), eClerx Services, BPCL, SBI Life Insurance, IIFL Finance, Cummins India, Laurus Labs, and Polycab India. The rally in PSU and energy stocks indicated strong investor confidence in these sectors, supported by policy tailwinds and better earnings outlooks.

Technical View: Is the Market Losing Steam?

According to Nagaraj Shetti, Senior Technical Research Analyst at HDFC Securities, profit-booking continued for the second consecutive session on Thursday, signaling that the market might be entering a short-term consolidation phase.

He noted that although the Nifty opened on a positive note, it failed to sustain its early momentum and declined steadily during the mid-session, eventually extending losses in the closing hours. On the daily chart, the Nifty formed a long bear candle — a sign of continued weakness — though it managed to hold above its immediate support levels.

Shetti added that the index is currently moving within a broad trading range between 26,100 and 25,700, with the trend now slightly tilted downward. “Technically, the short-term trend of the Nifty looks weak, but the medium-term outlook remains positive,” he explained. “If the index falls below the 25,700 level, strong support is expected near 25,500, from where a rebound could be seen next week. On the upside, 26,100 acts as an immediate resistance level.”

Analyst Insight: Cautious Optimism Amid Short-Term Weakness

Echoing similar sentiments, Rupak Dey, Senior Technical Analyst at LKP Securities, observed that the Nifty’s inability to hold above 25,950 has given bears a tactical advantage. “The index remained weak throughout the session as selling pressure intensified once the key support at 25,800 was breached,” Dey said.

According to him, the short-term trend remains bearish, with the possibility of a further decline toward 25,525. However, if the Nifty manages to reclaim and sustain above 25,850, it could signal a resumption of upward momentum. “Until then,” he noted, “traders should remain cautious and avoid aggressive long positions.”

Dey added that momentum indicators, such as the Relative Strength Index (RSI), are showing signs of mild exhaustion after the recent rally, suggesting a period of sideways consolidation or mild correction before the next leg higher.

Global and Domestic Cues

The weakness in Indian markets also mirrored a soft tone in global equities. Global investors have turned cautious ahead of upcoming central bank meetings and geopolitical developments. US Treasury yields remained elevated, while crude oil prices hovered near recent highs, keeping inflation concerns alive.

Domestically, investors are also digesting the corporate earnings season, which has produced a mixed bag of results. While sectors like banking, infrastructure, and capital goods have performed strongly, others like pharma and IT have lagged due to margin pressures and weak export demand.

Additionally, foreign institutional investors (FIIs), who were net buyers earlier in the month, turned net sellers in the last few sessions, contributing to the market’s pullback. However, domestic institutional investors (DIIs) continued to support the market, limiting the downside.

What to Watch for on November 3rd

Looking ahead to November 3rd, market sentiment will likely hinge on a combination of global cues, institutional flows, and technical levels. Traders will watch whether the Nifty can hold above the 25,700–25,500 support zone, as a decisive break below could trigger further weakness. Conversely, a strong rebound above 25,850–26,000 may reignite bullish momentum.

Investors should also keep an eye on sectoral rotation — particularly in PSU banks, defense, and capital goods — as these segments continue to show resilience. Meanwhile, IT and pharma stocks could remain under pressure unless there is a recovery in global demand signals.

Volatility may remain elevated as traders adjust their positions ahead of the new trading week and upcoming macroeconomic data.

In summary, while the market’s short-term tone has turned cautious after a stellar four-week rally, the medium-term outlook remains constructive. Strong domestic fundamentals, steady earnings growth, and policy support could help the market stabilize and resume its upward trajectory once the current phase of consolidation runs its course.