Sensex Down 519 Points.nifty at 25,597; Nifty Prediction for Tomorrow

Market Wrap: Indices Slip Ahead of Short Trading Week — What to Expect on November 5

The Indian stock market ended in negative territory on November 4, weighed down by broad-based selling pressure across most sectors. After showing resilience in the early part of the session, both benchmark indices succumbed to selling in the second half, closing with moderate losses. The Nifty 50 settled below the 25,600 mark, while the Sensex fell by over 500 points, reflecting cautious sentiment among investors amid global uncertainty and anticipation of key domestic triggers later in the week.

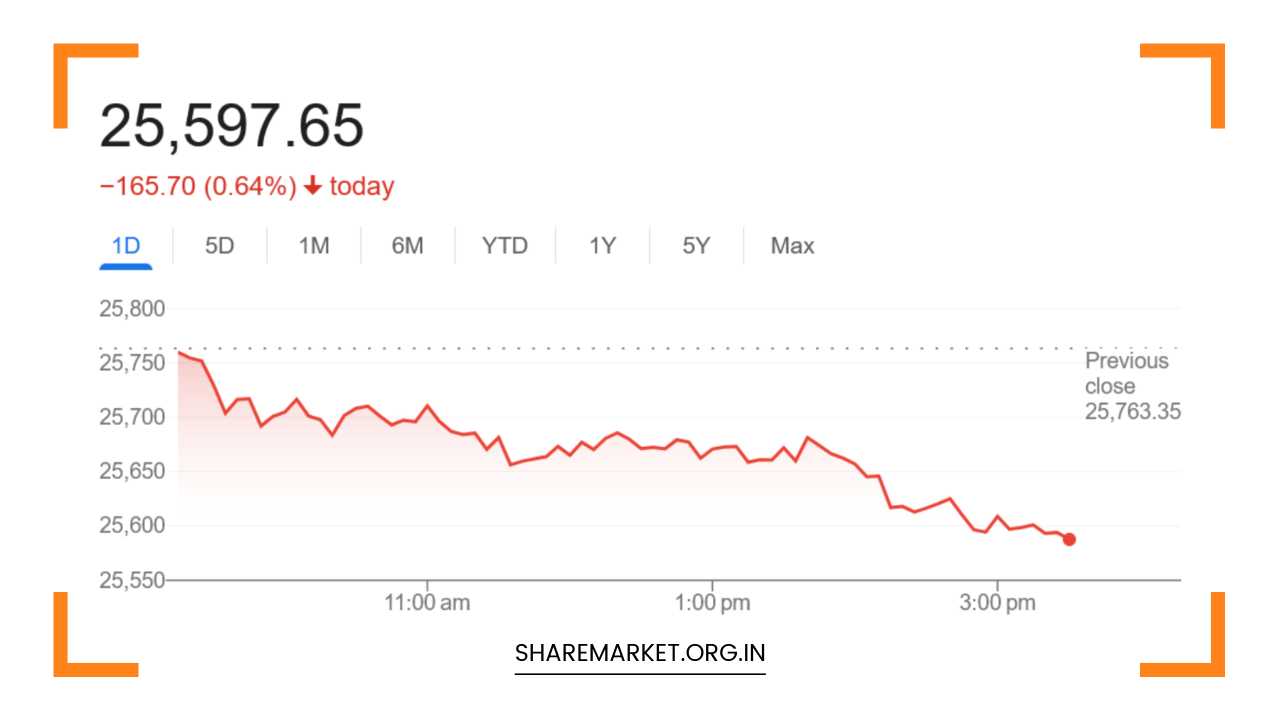

At the close of trade, the BSE Sensex dropped 519.34 points, or 0.62 percent, to 83,459.15, while the Nifty 50 declined 165.70 points, or 0.64 percent, to 25,597.65. Market breadth favored the bears — out of the total shares traded on the BSE, 1,543 stocks advanced, 2,439 declined, and 152 remained unchanged, indicating weak participation on the buying side.

Sectoral Overview: Broad-Based Selling, Limited Bright Spots

Sectorally, the weakness was widespread. Except for consumer durables and telecom, all other indices on the NSE closed in the red. The IT, auto, FMCG, metal, power, realty, and PSU indices saw declines ranging between 0.5% and 1%, indicating profit booking after a steady upward run in recent sessions. The BSE Midcap Index slipped 0.2%, while the Smallcap Index declined 0.7%, suggesting that broader market sentiment remained subdued.

Among the Nifty 50 constituents, the top laggards included Power Grid Corporation, Coal India, Tata Motors Passenger Vehicles, Bajaj Auto, and Eternal, which faced selling pressure amid sector-specific concerns and valuation-related profit booking. On the flip side, Titan Company, Bharti Airtel, Bajaj Finance, HDFC Life, and Mahindra & Mahindra (M&M) emerged as notable gainers, lending partial support to the benchmark index.

The slight outperformance of telecom and consumer durables stocks hinted at selective buying in defensives and consumption-driven segments, possibly as investors rotated funds away from cyclical sectors that have rallied sharply in the past month.

Technical Outlook: A Phase of Consolidation Before the Next Leg Higher?

From a technical standpoint, analysts suggest that the market’s current pause could be a healthy consolidation within a broader uptrend. According to experts at ICICI Securities, the Nifty’s recent stagnation is not a sign of weakness but rather a preparatory phase for the next upward move. They emphasize that the ongoing consolidation offers buying opportunities for investors with a medium-term perspective.

“The Nifty appears to be in a consolidation band between 26,100 and 26,700, which forms part of its structural uptrend,” analysts from ICICI Securities noted. “Once this phase concludes, the index is likely to regain momentum and could gradually advance towards its all-time high of 26,300 within this month.”

They recommend a buy-on-dips strategy, particularly in quality large-cap names that have shown resilience during recent market corrections. Sectors such as financials, infrastructure, and consumption may lead the next leg of the rally once the current consolidation ends.

Fundamental and Global Triggers: Eyes on Corporate Earnings and FII Flows

On the macroeconomic and fundamental side, Abhinav Tiwari, Research Analyst at Bonanza Portfolio, pointed out that global events and foreign investment flows will continue to exert significant influence on market sentiment in the coming sessions. “Volatility is likely to persist as investors assess mixed global cues, ranging from geopolitical tensions to shifting expectations around interest rate policies by major central banks,” Tiwari explained.

He also highlighted that the corporate earnings season remains a crucial near-term trigger. Several large-cap companies are scheduled to announce their Q2 results later this week, and these earnings will provide clearer insights into demand recovery, margin performance, and overall business sentiment across key sectors.

Additionally, the upcoming Guru Nanak Jayanti holiday will shorten the trading week, potentially leading to thin liquidity and exaggerated price movements as traders adjust positions ahead of the midweek break. This may add an element of volatility to intraday trading, especially in derivative-heavy counters.

Key Levels to Watch: Support and Resistance Zones

Providing a more granular technical outlook, Sudeep Shah, Head of Technical and Derivative Research at SBI Securities, outlined critical levels that traders should monitor closely. According to him, the Nifty has strong support between 25,480 and 25,440, and a further cushion at 25,310. On the higher side, immediate resistance is expected around 25,820-25,840.

“A decisive breakout above 25,840 could open the doors for the index to test the 25,960 level in the near term,” Shah said. “Until then, the market is likely to remain range-bound with a mildly positive bias.”

Turning to the Bank Nifty, Shah observed that the index has shown relative strength compared to the broader market, aided by buying interest in public sector banks (PSBs). The Bank Nifty has been trading within a tight range on the daily chart, indicating a phase of consolidation. Going forward, Shah identified the 57,450–57,400 zone as a strong support area, while resistance is likely around 58,250–58,350. A breakout above 58,350, he noted, could propel the index towards 58,800 in the short term, particularly if PSU banks continue to attract inflows.

Market Sentiment and Prediction for November 5

Looking ahead to November 5, market sentiment is expected to remain cautious but opportunistic. While technical indicators suggest that indices are nearing support levels, traders are likely to remain watchful of global cues — particularly movements in U.S. bond yields, oil prices, and foreign institutional investor (FII) activity. A pickup in FII inflows, combined with positive domestic earnings, could help the market stabilize and potentially trigger a recovery.

Domestic investors, meanwhile, may continue to focus on stock-specific action, especially in sectors showing resilience such as telecom, financial services, and consumer durables. Analysts recommend maintaining a balanced portfolio approach, combining defensive plays with selective exposure to high-conviction growth stories.

In summary, while Monday’s decline reflects short-term profit booking and caution ahead of event-heavy days, the medium-term market structure remains intact. With supportive domestic fundamentals, improving corporate earnings, and stabilizing global macro trends, the Indian equity market appears poised for renewed momentum once the current consolidation phase concludes.