Sensex Gain 105 Points, Nifty at 24,414; Tomorrow Nifty Prediction

Stock Markets Close Higher Despite Volatility; Geopolitical Concerns Could Drive Movement on May 8

Indian equity markets closed in positive territory on May 7, 2025, following a volatile trading session that saw benchmarks fluctuate amid geopolitical concerns and sector-specific activity.

The session reflected investor caution following India’s military operations against cross-border terrorism, yet broader market sentiment remained surprisingly resilient.

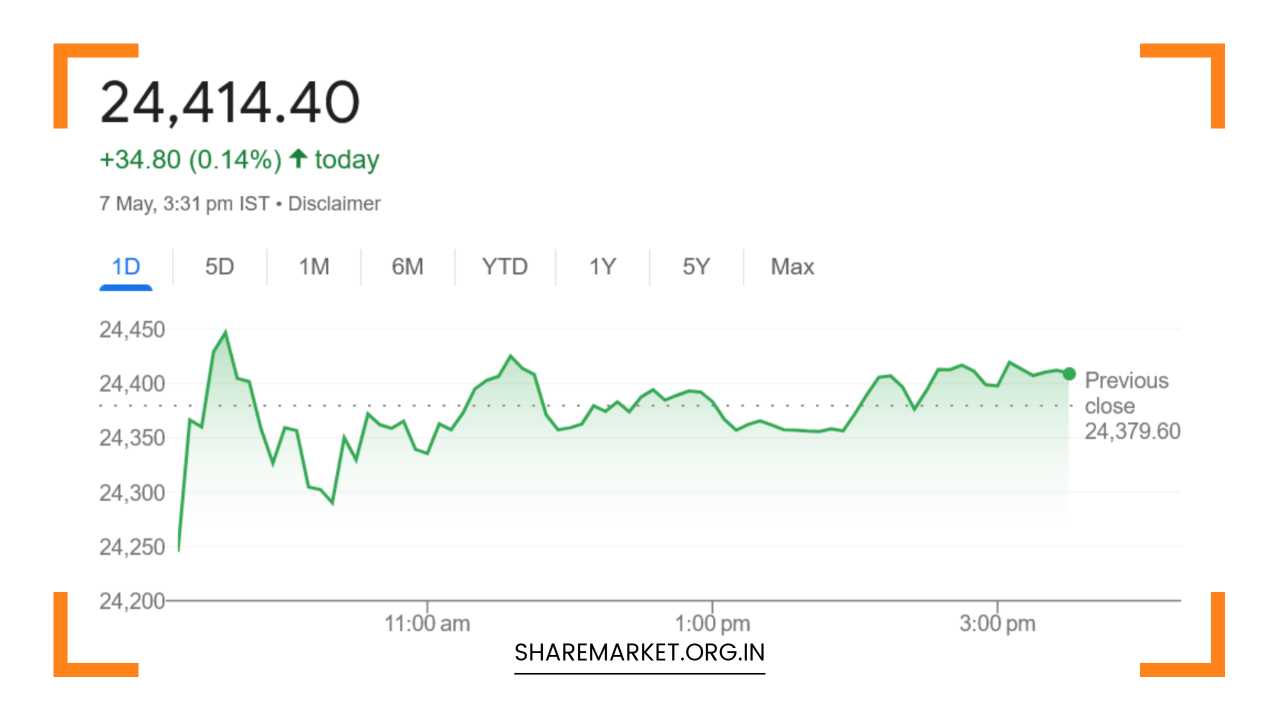

The Nifty50 ended the day up 34.80 points, or 0.14%, to close at 24,414.40. The BSE Sensex added 105.71 points, or 0.13%, to settle at 80,746.78.

The indices remained range-bound for much of the day after showing early signs of weakness, before staging a mild recovery in the afternoon.

Market Breadth and Sector Performance

Market breadth favored the bulls, with 2,121 stocks advancing, 1,620 declining, and 149 remaining unchanged on the BSE.

This broad-based participation was largely driven by buying interest in mid-cap and small-cap stocks. The BSE Midcap index rose 1.3%, while the BSE Smallcap index gained 1%, both outperforming the headline indices.

Among the sectoral indices, all but FMCG and Pharma closed in the green. Notable gainers included Auto, Media, Realty, and Consumer Durables, each posting gains of over 1%.

The Auto index, in particular, has continued its recent upward momentum, driven by robust sales data and optimism around sectoral growth.

FMCG and Pharma, on the other hand, underperformed. Some profit booking was seen in Pharma stocks after a decent run in previous sessions, while FMCG saw muted investor interest amid rising input costs and subdued demand signals.

Top Gainers and Losers

On the Nifty50, Tata Motors, Bajaj Finance, Jio Financial, Shriram Finance, and Eternal were the top performers.

Tata Motors saw a strong uptick driven by investor optimism surrounding its proposed corporate restructuring and expectations of continued demand in both domestic and export markets.

On the flip side, Asian Paints, Sun Pharma, Bajaj Auto, Grasim Industries, and Reliance Industries were among the biggest laggards, with profit-taking seen in several of these heavyweight stocks.

Military Action and Market Sentiment

A key source of intraday volatility was the ongoing military operation by India targeting cross-border terrorist camps.

While such actions typically rattle market sentiment, the Indian markets have so far responded with a mix of caution and resilience.

According to market analysts, the immediate impact of such geopolitical developments tends to be short-lived unless the conflict escalates significantly.

Prashanth Tapse, Senior VP at Mehta Equities, commented that markets were jittery earlier in the day due to the military news flow, but gradually stabilized as clarity emerged and risk appetite returned.

“Though the overall market closed with modest gains, we expect the geopolitical tension to continue playing a role in short-term market volatility. Investors should stay alert and avoid aggressive positioning in such an environment,” he said.

Technical View: Support and Resistance Levels

Aditya Gaggar, Director at Progressive Shares, highlighted that the Nifty traded within a limited range for most of the session after recovering from early lows.

He pointed out that the index faced resistance near the 24,500 mark, while support remains strong around 24,250.

“A decisive breakout above 24,500 could pave the way for a fresh rally, potentially taking the Nifty closer to the 24,700–24,800 zone. Conversely, any dip below 24,250 could invite selling pressure and drag the index lower,” Gaggar explained.

From a technical standpoint, broader participation by mid-cap and small-cap stocks is encouraging, signaling underlying strength. However, traders should remain cautious near key resistance levels.

Market Prediction for May 8: Stock-Specific Action Likely

Looking ahead to May 8, market watchers expect stock-specific activity to dominate, particularly in light of ongoing earnings announcements and sectoral developments.

Analysts caution that while index levels may appear stable, intra-day swings could be sharp, driven by reactions to news headlines and corporate results.

With India-Pakistan tensions still simmering in the background, there may be periods of nervousness.

Defensive sectors like IT and consumer staples could see renewed interest if risk aversion rises, while high-beta sectors like banking and real estate may remain volatile.

Another point of focus for investors will be the flow of institutional money. Foreign institutional investors (FIIs) have been net sellers in recent sessions, while domestic institutional investors (DIIs) have provided some support to the markets. Sustained buying or selling from these players can significantly influence near-term direction.

Investment Strategy

In this environment, analysts recommend a cautious yet selective approach. Investors are advised to focus on high-quality stocks with strong fundamentals, while keeping some cash ready to take advantage of dips.

For traders, adhering strictly to stop-loss levels and avoiding over-leveraged positions is essential.

Sectors such as auto, capital goods, and select financials continue to show strength and may offer opportunities in the near term.

However, traders should be prepared for rapid shifts in sentiment, especially if geopolitical conditions deteriorate or macroeconomic data surprises on the downside.

Key Takeaways:

- Indian stock markets ended with marginal gains despite initial weakness.

- Broader markets outperformed, led by strong buying in mid- and small-cap stocks.

- Auto, Realty, and Media sectors led the gains; FMCG and Pharma lagged.

- Military developments across the border added a layer of uncertainty.

- Technical charts indicate Nifty support at 24,250 and resistance at 24,500.

- Volatility likely to persist in the near term, with stock-specific action dominating.