Sensex Gain 319 Points, Nifty at 25,574; Nifty Prediction for Tomorrow

Sensex and Nifty End Three-Day Losing Streak: What to Expect on November 11

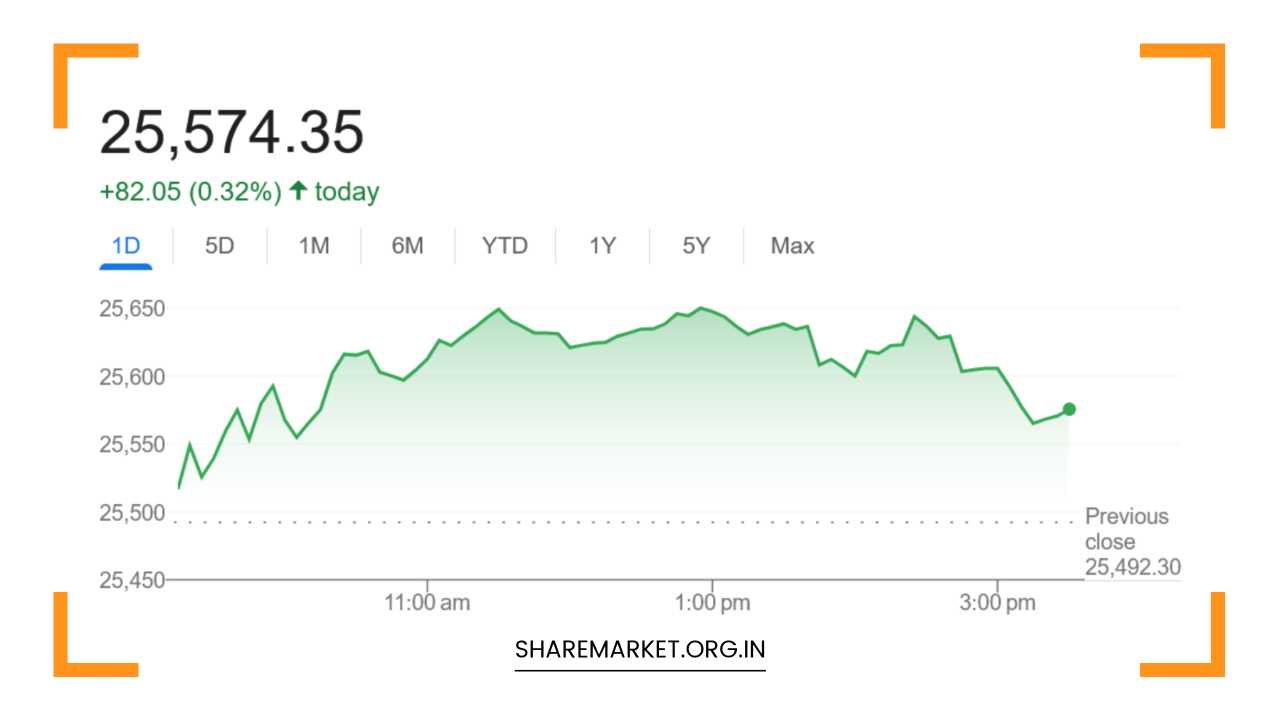

Market Today:

After three consecutive sessions of weakness, Indian equity benchmarks rebounded on Friday, November 10, ending the week on a positive note. The Nifty 50 managed to close above the key 25,550 level, while the Sensex regained momentum and finished the session with modest gains. Improved investor sentiment, selective buying in heavyweight stocks, and positive global cues helped lift market mood, although overall breadth remained somewhat mixed.

At the close of trade, the Sensex rose 319.07 points, or 0.38%, settling at 83,535.35, while the Nifty 50 advanced 82 points, or 0.32%, to close at 25,574.30. Market breadth on the Bombay Stock Exchange showed 1,787 stocks advancing, 2,183 declining, and 132 remaining unchanged, reflecting continued volatility and selective participation.

From a sectoral perspective, all major indices ended in the green except for the media index, which slipped around 1% due to profit booking in key names. The IT index emerged as the top performer of the day, rising 1.6%, buoyed by buying in frontline tech stocks such as Infosys, HCL Technologies, and Wipro. The pharma and metal indices also contributed positively, gaining nearly 1% and 0.6% respectively.

The BSE Midcap Index rose 0.6%, indicating that investors continued to show selective interest in quality mid-tier names. However, the Smallcap Index fell 0.4%, suggesting that risk appetite in smaller companies remains subdued amid ongoing global uncertainty and valuation concerns.

Among individual stocks, Infosys, HCL Technologies, Grasim Industries, Bajaj Finance, and Wipro were the top gainers on the Nifty. On the other hand, Trent, Apollo Hospitals, Max Healthcare, Power Grid, and Tata Consumer Products featured among the top laggards, reflecting profit booking in previously strong counters.

What Drove the Market on Friday

Market recovery on November 10 was largely driven by renewed optimism in technology and banking shares, following a period of consolidation. Traders cited improved global sentiment and easing concerns over foreign outflows as factors that helped Indian markets find support near recent lows.

Globally, investors appeared to be regaining confidence after a mild correction in U.S. equities earlier in the week. Bond yields in the U.S. stabilized, and oil prices remained range-bound, which provided a degree of comfort to emerging markets like India. A softer U.S. dollar also aided foreign inflows into domestic equities.

Meanwhile, the rupee traded within a narrow range against the dollar, reflecting relative stability in the foreign exchange market. However, analysts continue to caution that global macroeconomic headwinds—such as uncertainty over interest rate paths in major economies and geopolitical risks—could continue to influence short-term market movements.

Expert Views: What to Expect Next

Market experts remain divided about the near-term outlook, even as India’s long-term growth story remains robust. V.K. Vijayakumar, Chief Investment Strategist at Geojit Financial Services, noted that India’s corporate earnings growth remains healthy and is expected to accelerate in the coming quarters. “The Indian economy continues to demonstrate resilience, with several sectors showing consistent improvement. Strong earnings momentum, coupled with structural reforms and policy stability, should support market strength in the medium term,” he said.

However, Vijayakumar also warned that the global technology rally, driven by artificial intelligence (AI) euphoria, may be approaching a point of exhaustion. “The AI bubble appears to be nearing saturation, and a potential correction in global tech stocks could drive foreign institutional investors (FIIs) to reallocate funds toward emerging markets like India,” he explained. This rotation could act as a tailwind for Indian equities in the months ahead.

Investors are advised to keep a close watch on key sectors such as banking and finance, telecom, capital goods, defense, and automobiles, which are expected to benefit from strong domestic demand, government spending, and an improving credit cycle.

Technical Outlook: Key Levels to Watch

From a technical perspective, the Nifty remains locked in a narrow trading band, and traders are awaiting a clear breakout to determine the market’s next major move. Analysts believe that 25,800–25,900 is the crucial resistance zone for the index. A decisive move above this level could trigger short-covering and pave the way for renewed bullish momentum. Conversely, sustained weakness below 25,400 could invite further selling pressure and extend the ongoing corrective phase.

Dhupesh Dhameja, Derivatives Research Analyst at Samco Securities, noted that short sellers remain active and are likely to use intraday rallies as opportunities to build positions until the Nifty convincingly reclaims the 25,800–25,900 range. “A strong close above this level could neutralize the current bearish sentiment and potentially spark a near-term rally. However, if the index fails to hold above support levels, we could see an extended consolidation phase,” Dhameja said.

In derivatives data, analysts observed a buildup of open interest in both call and put options near the 25,600–25,800 strike range, suggesting indecision among traders about the index’s next directional move. Volatility, as measured by India VIX, remained subdued but could rise if the index fails to maintain its recent gains.

Broader Market Sentiment and Strategy

For investors, the recent volatility offers a reminder of the importance of maintaining a disciplined and diversified approach. Experts suggest focusing on high-quality companies with strong balance sheets, sustainable earnings visibility, and sectoral tailwinds.

Short-term traders, on the other hand, should monitor global cues—especially movements in U.S. yields, crude oil prices, and foreign fund flows—as these continue to influence domestic sentiment. With the earnings season largely behind, attention may shift toward macroeconomic data, including inflation numbers and industrial output, which could provide further clarity on policy direction.

While markets could remain range-bound in the immediate term, the overall setup continues to favor a “buy-on-dips” strategy for long-term investors, especially in sectors aligned with India’s growth story such as infrastructure, manufacturing, defense, and renewable energy.

Market Prediction for November 11

Heading into the next trading session on November 11, analysts expect a cautious start amid mixed global signals. The focus will remain on whether the Nifty can build on Friday’s recovery and test the 25,800 resistance zone. If buying momentum extends, particularly in IT, banking, and capital goods sectors, the market could witness a short-term uptrend. However, any failure to sustain above 25,550 may invite renewed selling pressure.

In summary, while the near-term outlook remains uncertain, underlying fundamentals, corporate earnings strength, and a stable macroeconomic backdrop continue to lend support to Indian equities. Market participants are advised to remain selective, avoid aggressive leverage, and stay tuned for clearer directional cues in the coming sessions.