Sensex Gain 446 Points, Nifty at 24,821; Nifty Prediction for Tomorrow

Markets Close Higher: What to Expect on July 30

Indian equity benchmarks ended with solid gains on July 29, reversing some of the recent weakness driven by global uncertainty and persistent foreign institutional investor (FII) selling.

A positive trend across sectors, supported by buying in heavyweights, lifted sentiment ahead of a key earnings week and global economic developments.

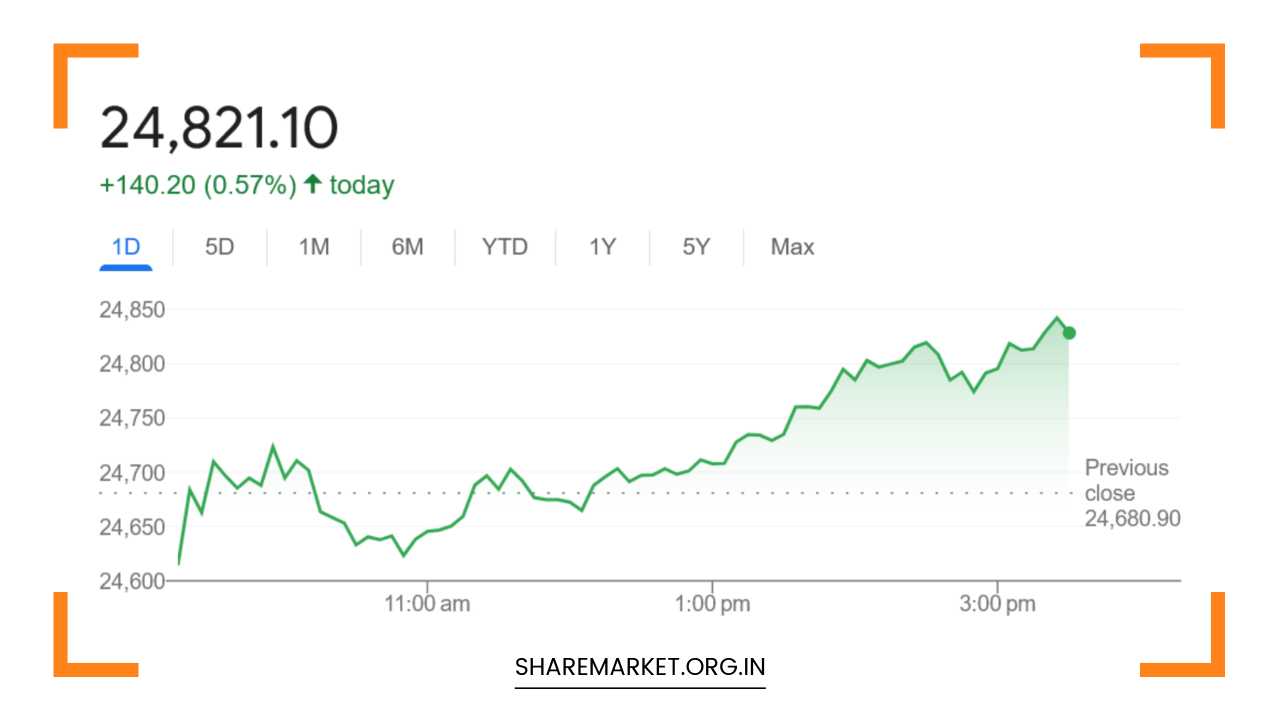

The Nifty 50 closed 140.20 points or 0.57% higher at 24,821.10, crossing the 24,800 mark, while the Sensex advanced 446.93 points or 0.55% to end at 81,337.95.

The gains were broad-based, with both mid- and small-cap indices outperforming. The BSE Midcap Index rose 0.8%, and the Smallcap Index posted a 1% gain, reflecting strong participation from retail and domestic investors.

Broad Market Performance

Market breadth favored the bulls, with 2,399 stocks advancing, 1,451 declining, and 141 remaining unchanged. The buying interest was widespread, cutting across sectors and market capitalizations.

All sectoral indices on the BSE and NSE closed in the green, with the realty, pharma, oil & gas sectors gaining around 1% each.

Defensive sectors like pharmaceuticals attracted safe-haven buying amid ongoing global concerns, while real estate and energy saw momentum driven by improving domestic demand and firm crude prices.

Key Movers

On the Nifty, Reliance Industries, L&T, Asian Paints, and Eicher Motors were among the top gainers, driving index gains through a combination of value buying and strong fundamentals.

Reliance gained on expectations of robust quarterly results, while L&T and Asian Paints advanced on steady institutional interest.

On the flip side, SBI Life Insurance, TCS, Axis Bank, HDFC Life, and Titan were among the top laggards.

These stocks saw profit-booking following recent rallies, and in the case of some financials, investor caution ahead of quarterly earnings weighed on sentiment.

Expert Commentary and Market Sentiment

Market analysts believe that despite Monday’s rebound, caution remains warranted due to a number of unresolved macroeconomic risks.

According to VK Vijayakumar, Chief Investment Strategist at Geojit Financial Services, the underlying market sentiment is mixed, as global uncertainty and foreign selling pressure continue to weigh on confidence.

“There are currently more unfavorable conditions than favorable ones for the market,” said Vijayakumar.

“The absence of a finalized trade agreement between India and the US before the August 1 deadline, coupled with sustained foreign institutional investor selling, is limiting market upside.

However, domestic institutional investors (DIIs) have remained active and supportive, preventing a sharper correction.”

This cautious optimism is echoed by Vaibhav Vidwani, Research Analyst at Bonanza Portfolio, who noted that markets are likely to remain range-bound with an upward bias, provided corporate earnings meet expectations.

“The market is holding onto cautious optimism. In an environment filled with macroeconomic uncertainties, the attention will naturally shift to company earnings. Investors will be closely tracking Q1 results to gauge future growth prospects,” Vidwani said.

Trade Deal and External Pressures

A key overhang for the market remains the pending trade negotiations between India and the United States.

With the deadline for a limited trade agreement set for August 1, the absence of a resolution continues to be a source of concern.

Investors fear that without progress, retaliatory tariffs or delays in easing trade restrictions could dampen exports and disrupt cross-border investment flows.

Additionally, sustained foreign portfolio investor outflows continue to exert pressure. In recent weeks, FIIs have been consistent sellers, influenced by global risk aversion, rising US bond yields, and concerns about emerging market valuations.

This has been partly offset by buying from DIIs and retail investors, but analysts warn that a reversal in DII sentiment could expose the market to heightened volatility.

Domestic Fundamentals and Earnings

Despite the external pressures, domestic fundamentals remain largely stable. India’s economic growth projections for FY26 remain in the range of 6.5% to 7%, supported by robust tax collections, healthy corporate balance sheets, and resilient consumer demand.

Inflation remains within the Reserve Bank of India’s target band, though food price volatility continues to be a watchpoint.

With the earnings season gaining momentum, market participants are looking for clarity on corporate performance, particularly in sectors like banking, consumer goods, auto, and IT. Companies that beat expectations could drive the next leg of the rally, while disappointing numbers could trigger profit-taking.

The outlook for financials will be critical, especially given the recent outperformance in large private sector banks and insurance companies.

Similarly, IT companies, which have seen mixed results, will be watched closely to assess the impact of global tech spending and margin pressures.

Global Factors

Global cues will continue to play a crucial role in shaping sentiment. Investors are monitoring the US Federal Reserve for any signals regarding interest rate cuts later this year.

Additionally, upcoming economic data from China and geopolitical developments in Europe and the Middle East could sway investor risk appetite.

US and European markets showed mixed trends in the previous session, and Asian markets remain volatile.

A stabilizing global backdrop could support emerging markets like India, but any resurgence of risk-off sentiment globally would weigh on Indian equities, especially those with high foreign ownership.

What to Watch on July 30

Going into the July 30 session, investors are likely to focus on:

- Q1 earnings reports, especially from large-cap names

- Progress or breakdown in India-US trade talks ahead of the August 1 deadline

- FII and DII investment flows, which remain crucial for market direction

- Global market cues, including US macro data and Asian indices

- Movement in the Indian rupee and bond yields

Given the current backdrop, a cautious but optimistic tone may continue to dominate. Short-term rallies are likely to be influenced by stock-specific news and earnings surprises, while any deterioration in external conditions could cap upside momentum.

Final Thoughts

Monday’s session brought a much-needed relief rally to the Indian equity market, but risks remain. While strong domestic inflows and sectoral strength have provided a cushion, global uncertainty and trade-related tensions continue to keep investors on edge.

For now, the market appears to be in a wait-and-watch mode. Investors would be wise to remain selective, focus on fundamentally strong companies, and track macro developments closely.

With the earnings season in full swing and trade policy decisions looming, the next few sessions could prove pivotal in shaping near-term market direction.