Aastha Spintex IPO Listing: Stock Lists at 4.41% Discount on BSE

Aastha Spintex IPO Listing: ₹136 Share Fails to Turn an Initial Profit, but Company Profits Grow at Rocket Speed

The domestic textile landscape witnessed a highly anticipated debut as Gujarat-based cotton yarn manufacturer Aastha Spintex Limited officially entered the public markets. Despite capturing significant investor interest during its bidding window, the stock’s market debut on the premier exchanges delivered an unexpected plot twist. Belying positive expectations and minor premiums observed in the grey market, the stock failed to turn an immediate profit for allotment winners on listing morning. However, underneath the lukewarm market reception lies a company whose operational metrics and net profits have been growing at an astonishingly high velocity.

The Listing Day Dynamics: From Initial Discount to Upper Circuit Recovery

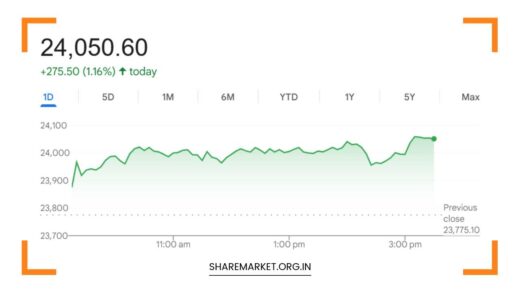

Aastha Spintex shares made a dual entry on the Bombay Stock Exchange (BSE) and the National Stock Exchange (NSE). The initial public offering (IPO) had set its final issue price at the upper limit of its price band at ₹136 per share.

The Morning Slump

When the pre-open discovery session concluded, the shares listed on both the BSE and NSE at a flat ₹130.00. This opening price represented a direct 4.41% capital discount relative to the issue price. For short-term traders and retail investors who aggressively bid for the issue purely in anticipation of listing-day windfalls (listing gains), this flat-to-negative start was a stark reminder of equity market volatility.

The Intraday Resurgence

The narrative shifted as regular trading hours advanced. Instead of triggering a cascading sell-off, the lower price entry points appeared to attract value-oriented buyers who recognized the company’s strong underlying financial performance.

After initially consolidating and advancing with minor tick-by-tick gains, structural buying momentum picked up significantly. The stock steadily recovered all of its lost ground, ultimately hitting its daily upper circuit limit of ₹136.45 on the BSE. By locking into the upper circuit and closing the day at that exact level, the stock managed to rescue the day for original allottees.

By the closing bell of its first trading day, IPO investors found themselves marginally in the green, securing a 0.33% gain over their initial capital layout.

Subscription Footprint: How Investors Responded

Prior to listing, the ₹170 crore book-built public issue was open for subscription from June 29 to July 1. Backed by its lead managers, the issue saw robust aggregate demand across all investment blocks. The 100% fresh issue of 1.25 crore equity shares generated a cumulative subscription rate of 5.05 times the total shares on offer.

The structural appetite across individual investor categories can be broken down as follows:

| Investor Category | Subscription Multiplier | Institutional & Retail Behavior |

| Non-Institutional Investors (NII/HNI) | 8.29x | Led the charge, demonstrating aggressive high-net-worth individual demand. |

| Qualified Institutional Buyers (QIBs) | 3.59x | Formed a stable foundational bidding layer (excluding anchor allocations). |

| Retail Individual Investors (RII) | 2.54x | Displayed measured participation, with a minimum lot investment of 110 shares costing ₹14,960. |

| Employees | 5.43x | Strong internal backing showcasing confidence from within the workforce. |

Strategic Capital Deployment: Where Will the ₹170 Crore Go?

Unlike issues dominated by an Offer for Sale (OFS)—where existing promoters cash out—Aastha Spintex structured its public debut entirely around a fresh capital issue. This implies that every rupee raised minus statutory issue expenses flows directly onto the company’s balance sheet to fuel inorganic growth.

The corporate layout for the net proceeds targets explicit expansionary mandates:

-

Acquisition of Falcon Yarns Private Limited (₹111.51 crore): The primary chunk of the IPO proceeds is earmarked as part-payment to acquire Falcon Yarns. This strategic move is poised to transform Aastha’s operational scale, effectively more than doubling its production capacity from 7,700 MT to an estimated 17,457 MT per annum.

-

Working Capital Infusion (₹10.00 crore): To ensure that the newly acquired Falcon Yarns entity integrates smoothly without choking the parent firm’s liquidity, ₹10 crore will be disbursed via inter-corporate deposits to support its immediate working capital needs.

-

General Corporate Purposes & Expenses (Remaining Balance): The residual capital will fund ongoing organizational optimization, brand building, and generic corporate overheads, ensuring the broader corporate machine remains adequately capitalized.

About Aastha Spintex: Operational Strengths & Business Model

Established in 2013 and guided by Promoter and Managing Director Patel Divyang Jashvantbhai, Aastha Spintex has carved out a distinct identity within the textile B2B ecosystem. The company specializes in the manufacturing and trading of multiple high-demand cotton variants:

-

Carded Yarn: Known for its breathability and foundational texture, widely used in standard garments.

-

Combed Yarn: A smoother, tougher variety where short fibers are combed out to produce high-quality apparel.

-

Compact Combed Yarn: Premium, low-fuzz yarn engineered for high-end luxury textiles.

The company operates a vertically integrated, semi-automated spinning and ginning manufacturing unit located in the Halvad region of the Morbi district in Gujarat.

Key Operational Facets

-

Dual-Use Cotton Bales: Aastha utilizes self-produced cotton bales as raw feed for its internal spinning lines to ensure strict quality control over its premium yarn output. Excess bale inventory is traded directly to external spinning mills across the region.

-

Sustainability Integration: Embracing circular economy principles, the plant recycles cotton yarn waste generated during the core textile phases, re-processing it into downstream commercial products.

-

Product End-Uses: The company’s outputs serve as building blocks across multiple consumer and industrial segments, including denim fabrication, terry towels, home textiles, sweaters, socks, and specialized industrial fabrics.

Rocket-Speed Financial Growth

While the stock market’s initial price discovery mechanism was cold, the internal accounting books tell an entirely different story. Aastha Spintex has displayed an exceptionally aggressive financial turnaround trajectory over the last three fiscal terms.

Historical Financial Performance

The company’s topline has expanded healthily, growing by roughly 21% inside a multi-year bracket to hit ₹352.17 crore in FY2025. However, it is the bottom-line profitability that exhibits a rocket-speed trajectory, jumping significantly from a modest net profit in FY2023 to strong double-digit figures by FY2025.

| Financial Metric | FY 2023 | FY 2024 | FY 2025 | 9 Months (FY 2026) |

| Total Revenue | ₹291.05 crore | ₹312.40 crore | ₹352.17 crore | ₹314.02 crore |

| Net Profit (PAT) | ₹1.06 crore | ₹16.29 crore | ₹22.92 crore | ₹17.56 crore |

This exponential growth curve highlights rapid margin expansion, shifting from a thin, asset-heavy survival margin to a much healthier post-tax profitability profile.

Recent Operational Momentum

The momentum has sustained well into the current operational cycle. Financial data covering the first 9 months of FY2026 (April–December 2025) indicates that Aastha Spintex secured an operational revenue of ₹314.02 crore alongside a strong net profit of ₹17.56 crore. Key structural ratios for this trailing period highlight solid operational efficiency, with an EBITDA Margin of 11.25%, a Return on Equity (ROE) of 12.80%, and a manageable Debt/Equity Ratio of 0.66.

Forward Outlook: What Should Investors Watch?

Aastha Spintex’s below-issue listing suggests that the public market valued the business with near-term caution, correcting its initial Price-to-Earnings (P/E) multiple downward from an IPO-level 25.65x to a slightly more reasonable 24.51x post-listing. This pricing places it at a noticeable discount compared to major industry peers, which float at an average group P/E closer to 43x.

Moving forward, the company’s long-term stock performance will likely be tied to its execution on three main fronts:

-

The Falcon Yarns Integration: The speed at which the company commercializes the Falcon Yarns acquisition to tap into greater economies of scale.

-

Geographical Diversification: Reducing its heavy geographic concentration, given that over 96% of its sales originate within Gujarat.

-

Cash Flow Management: Turning its strong paper accounting profits into positive operational cash flows, correcting the cumulative outflows experienced over the past few quarters.

For patient investors, the dramatic intraday recovery to the upper circuit indicates that while the stock failed to provide instant gratification, its deep fundamentals continue to command respect on Dalal Street.