Sensex Down 479 Points, Nifty at 23,913; Tomorrow Nifty Prediction

Market Slump on F&O Expiry: Sensex Sheds 479 Points, Nifty Slides Below 24,000; What to Expect on May 27

Indian equity benchmarks buckled under pressure on May 26, ending a highly volatile trading session firmly in the red. The losses coincided with the monthly Futures and Options (F&O) expiry, a day traditionally marked by heightened volume and aggressive position squaring. Compounding the technical pressure was a sudden flare-up in geopolitical tensions in the Middle East, which effectively choked off early market optimism.

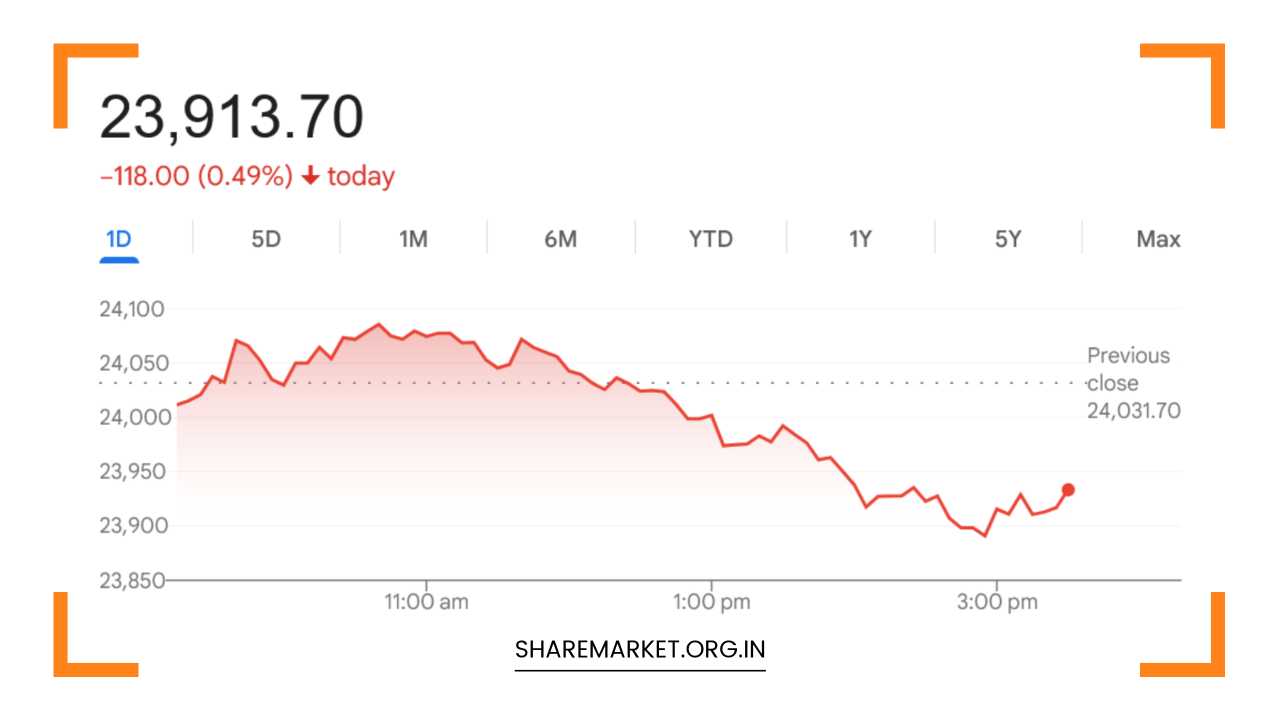

By the closing bell, the BSE Sensex tumbled 479.26 points, or 0.63%, to settle at 76,009.70. Similarly, the broader NSE Nifty 50 index shed 118 points, or 0.49%, to close at 23,913.70, failing to defend the psychologically crucial 24,000 mark.

Market Performance Snapshot

Despite the weakness in heavyweights, the broader market painted a contrasting picture of resilience. Small-cap and mid-cap stocks bucked the broader negative trend, indicating that domestic retail and institutional liquidity remains robust.

Benchmark Indices

-

BSE Sensex: Closed at 76,009.70, down 479.26 points (-0.63%)

-

NSE Nifty 50: Closed at 23,913.70, down 118.00 points (-0.49%)

-

Nifty Midcap: Closed up 0.50%

-

Nifty Smallcap: Closed up 0.35%

Top Gainers and Losers (Nifty 50)

-

Top Losers: Apollo Hospitals, Bharti Airtel, TCS, Wipro, and Trent led the laggards, facing severe profit-booking.

-

Top Gainers: Adani Enterprises, Tata Motors Passenger Vehicles, Tech Mahindra, Nestle, and Eternal managed to swim against the tide, logging decent gains.

Geopolitics and Expiry: The Twin Triggers

The market opening was relatively muted, but a modest recovery during the initial trading hour gave bulls some hope. However, this optimism evaporated rapidly due to shifting macroeconomic and geopolitical realities.

1. The US-Iran Flare-up

Early trading sentiment was supported by a glimmer of hope surrounding a potential diplomatic peace agreement between the US and Iran. This hope was swiftly crushed following reports of US military operations in southern Iran. The sudden escalation triggered an immediate knee-jerk reaction in global commodity markets.

2. Crude Oil & Currency Pressures

Crude oil prices witnessed an intraday spike following the geopolitical news, directly impacting net-importing economies like India. The sudden surge in oil prices erased early marginal gains achieved by the Indian Rupee, compounding worries over imported inflation and fiscal deficits.

3. Institutional Divergence (FII vs. DII)

The market layout continues to be a battleground between Foreign Institutional Investors (FIIs) and Domestic Institutional Investors (DIIs). Persistent selling pressure from FIIs weighed heavily on front-line banking and IT stocks. Conversely, steady inflows from DIIs acted as a crucial cushion, steering the mid-cap index to a new all-time high during intraday trade.

Expert Take: “The glimmer of hope regarding a potential peace agreement between the US and Iran quickly dissipated following reports of US military operations in southern Iran. This development triggered a sudden surge in crude oil prices and erased the marginal gains the Rupee had managed to secure. The monthly F&O expiry further intensified technical selling pressure. Despite this, mid-cap stocks demonstrated resilience, reflecting investor confidence in domestic earnings.”

— Vinod Nair, Head of Research at Geojit Investments

Technical Outlook for May 27

Nifty 50 View: Buy on Dips Remains the Play

Technically, the Nifty 50 closed near its intraday lows, right around the 23,900 level. The index is currently sandwiched between its 20-day and 50-day Exponential Moving Averages (EMA). Despite the day’s decline, the Moving Average Convergence Divergence (MACD) histogram continues to flash a positive crossover, indicating that the underlying medium-term bullish structure hasn’t broken down.

According to market analysts, low investor participation at higher levels hindered the pullback rally. However, the internal strength of the broader market suggests that structural damage is minimal.

-

The Upside Targets: Immediate resistance is pegged at the 24,000 to 24,050 zone. A decisive, sustained breakout above the 24,050 to 24,100 band could trigger a short-covering rally, driving the index toward 24,250, and subsequently 24,400.

-

The Downside Cushions: Immediate support rests within the 23,800 to 23,750 zone, closely aligned with the 20-DEMA and last week’s closing baseline. If selling intensifies, a critical foundational support line is placed at 23,600. Analysts suggest utilizing any dips into the 23,700 to 23,800 territory to accumulate quality stocks.

Bank Nifty View: Private Banks Take the Wheel

The banking index experienced a volatile session, opening on a positive note but stumbling twice at intraday resistance in the 55,500 to 55,550 range. Heavy profit-booking in the latter half dragged Bank Nifty down to close at 55,093, marking a loss of 0.36%.

The index failed to sustain above its 50-day EMA, signaling a temporary pause in its upward momentum. However, an analysis of the Relative Rotation Graph (RRG) presents a highly bifurcated internal sector outlook:

-

Private Banking Sector: Positioned firmly within the “Leading Quadrant,” indicating robust relative strength and strong upward momentum. Private banks are heavily favored to outperform the broader market in the upcoming sessions.

-

PSU Banking Sector: Lingering within the “Lagging Quadrant.” State-owned banking counters are expected to continue facing relative underperformance and selling pressure on rallies.

Key Levels for Bank Nifty on May 27:

-

Resistance: The 55,500 to 55,600 range serves as the immediate ceiling. If bulls clear this barrier, the index is poised to target 56,000 and 56,400.

-

Support: The 54,700 to 54,600 zone acts as the immediate demand area where buying interest is anticipated to emerge.

Trading Strategy & Sectoral Playbook

With the monthly F&O expiry out of the way, the market’s technical baggage is significantly lighter. However, external triggers will remain the primary drivers of market direction on May 27. Barring FMCG and Metals, most sectoral indices closed in the red on May 26, with Realty, Consumer Durables, and Banking slipping 0.5% to 1%.

Investors should consider the following tactical approaches for the upcoming sessions:

-

Deploy a “Buy-on-Dips” Strategy: The broader market’s refusal to correct alongside the front-line indices indicates substantial liquidity waiting on the sidelines. Dips toward 23,800 on the Nifty should be viewed as accumulation windows.

-

Focus on Relative Strength: Pivot away from lagging sectors like PSU Banks and specific IT counters facing headwinds. Allocate capital to private banking heavyweights and defensive plays like FMCG and Metals, which displayed relative outperformance during Tuesday’s sell-off.

-

Strict Risk Management: Given that global crude prices and geopolitical updates from the Middle East are highly fluid, sudden overnight gaps are entirely possible. Traders should avoid carrying highly leveraged overnight positions and maintain strict stop-losses.